Simon Quilty: Australia’s Feedlot Sector Goes On The Market

26 November 2025, AU: You could be mistaken in thinking that Australia’s feedlotting is seeing players exit the market due to difficult times. This could not be further from the truth.

In actual fact, it’s the opposite: profits are extremely robust, and feedlot space remains tight, as strong global demand, cheaper feed costs, and plentiful cattle supply have led to exceptionally good returns this year.

So, why the exodus?

In this report, Simon Quilty examines why key strategic feedlot assets have been put up for sale in recent months and how and why this is occurring.

Who has recently sold and who is on the market?

Recently sold: Rangers Valley Feedlot

The most recent sale was Rangers Valley, owned by Marubeni Corporation (a Japanese-based company), to Stanbroke Holding Company. The sale included the 40,000-head feedlot, as well as 40,000 head of fullblood and Wagyu X long-fed Angus and 4,900 ha of grazing and farmland, along with highly regarded export brands that are sold to 50 countries around the world.

Media estimates of the sale price are $400 million, but neither the buyer nor the seller has given an official figure.

Marubeni bought the feedlot in 1988, which was a 4,000-head feedyard at the time. This was Marubeni’s first investment in an integrated supply chain. It was a strategic investment made just prior to the liberalisation of the Japanese beef market in the mid-90s; their aim was to produce beef as an alternative to Japan’s domestic beef, which it achieved.

The decision to sell the operation is in line with their Mid-term Management Strategy, which is focused on ‘accelerating investment recovery and then prioritising capital allocations to high-quality growth investments.’

On the market: Mort & Co Pinegrove and Yarranbrook feedlots and Gogango (a greenfield proposed feedlot site)

The two feedlots have a combined capacity of 28,238 head, with Gogango having approval for 36,500 head.

It should be noted that the two existing feedlots have approval for an additional 27,862 head, bringing the three facilities’ potential capacity to 92,600 head.

The decision for Mort & Co to divest itself of these facilities is due to the minority shareholders of the group, who own 40 per cent of the business and want to exit their shareholdings. No different from Marubeni’s decision, these minor shareholders want to recover their investment so they can focus on other investments.

On the market: Elders Killara feedlot

The Killara feedlot has a capacity of 22,500 head, with a yearly turnoff of 65,000 head. The focus is on Angus and Wagyu feeding, with the majority company-owned and a small custom feeding component.

In addition, the feedlot owns/leases an adjacent 1,300 ha of both irrigated and dry-farming country, which produces feed for the feedlot, including hay and corn silage.

As part of this infrastructure is a 13,500-head-per-year grass-finishing operation that supplies Certified Grassfed beef to both domestic and export programs.

As part of the operation, a 500-kilowatt solar farm helps minimise energy costs.

Why the decision to sell? Feedlot evaluations lie at the heart of decisions.

The true driver of these feedlot sales and offerings is the recent changes in feedlot evaluation.

In the last 12 months, Queensland feedlot values have jumped from $1500 per steer area to $3000 per steer area. In NSW and Victoria, evaluations have risen even higher to $3500 to $4000 per steer area due to greater difficulty in obtaining permits and environmental approvals.

The revised evaluation levels are based on feedlot profitability, which has doubled over the past few years.

One effect of improved feedlot profitability is a reduction in custom feeding, as asset owners look to capitalise on their own investments.

This may lead to some potential problems in the future, particularly in Queensland, should conditions turn dry, and producers look to feedlots to mitigate drought risk. The ‘inn is full’ with most feedlots with sophisticated supply chains and dedicated cattle going to specific grain-fed markets.

It should be noted that Wagyu numbers on feed are starting to increase again, numbers may not be at their record levels again but they are definitely off the lows, and this long-term feedlot resident does tie up feedlot space.

So, any excess cattle turnoff due to dry conditions could lead to lower prices if they are not placed in feedlots. I see the north of Australia as far more vulnerable to this potential problem than southern Australia, where cattle numbers have been depleted.

Changing of the guard, more so than an exodus

When looking at the players involved, many of these investors do not have feedlotting as their core business. The divestment of their feedlot investment allows these investors to reallocate their profits to other parts of their own businesses.

The increase in feedlot valuations, as stated, led to this decision-making.

The likely buyers are significant players in the supply chain looking to further add value to their existing businesses.

Stanbroke is a good example that, in its own right, has forged a very strong global market platform and, with the acquisition of Rangers Valley, will strengthen this through Rangers Valley’s strong brand name, which complements Stanbroke’s equally strong reputation.

The premium end of the market is where the greatest complementary factors lie, with both companies having strong Wagyu and Angus feed programs. The ability to bring these programs under one roof offers advantages in scale, marketing options, and, most importantly, costs, enabling them to serve an even larger customer base with greater efficiencies.

The combined feedlot capacity of both Stanbroke and Rangers Valley is 90,000 head, over a broader geographical area across Central NSW and the Darling Downs, giving a wider procurement base across differing regions and herd types.

The acquisition of either the Mort & Co feedlots or Elders Killara is likely to be in the same vein, with the likely purchaser looking to add value to an existing supply chain participant that sees these assets as critical to its core business.

I believe the current changing of the guard with feedlot ownership is seeing those current owners/shareholders looking to divest themselves of assets that are not necessarily part of their core business today, that 20 years ago may have been, and as a result, these assets will go to other businesses that see these assets as central to their current businesses.

It should be noted that purchasing a feedlot at $3000 per steer area is still cheaper than building your own, and should you choose to develop a greenfield site, there is almost a 2-year delay until it is fully operational. In contrast, an already built feedlot has cash flow from

Why have these assets all appeared on the market at the same time?

As stated earlier, the re-evaluation of feedlot values has been the catalyst, giving many of these shareholders a chance to sell their assets at a good profit. Prior to these recent valuations, the opportunities to sell had been few and far between, so these recent increases in valuations now ensure a decent investment return.

What does the future look like for the feedlot sector?

The future looks good. I think one of the misconceptions is that the ‘exodus’ is due to rats leaving a sinking ship, with hard times ahead amid rising livestock prices.

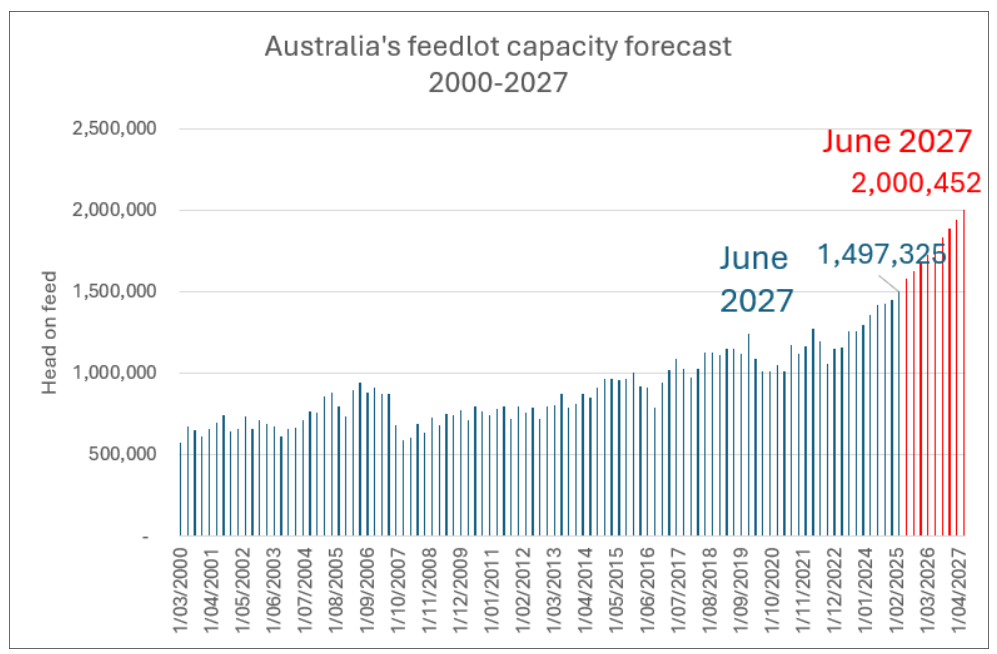

This could not be further from the truth. Australia’s feedlot sector is likely to continue its expansion, with I expect two million on feed by mid-2027. This will be driven by Australia’s backfilling role in global markets as the US beef supply tightens further.

Strong margins over the last year are expected to carry into 2026 and 2027 with subdued feed prices. Feed wheat is expected to remain at $300 to $350 per MT, delivered Darling Downs, for the next 6 to 12 months, supported by large global grain inventories.

US beef and cattle prices are expected to rise well into 2026, as their rebuild gets underway. So, higher global prices are expected in all markets where Australia competes with US beef.

The Achilles heel of Australia’s feedlot sector and processing sector will be higher Australian cattle prices over the next two years as Australia moves into a rebuild.

This does work into the feedlot sector’s hands as they ‘trade from the long side’ and will be able to take advantage of the four-to-six-month period of the buy time versus the sell time in a rising market.

During periods of tight supply, the tendency is for animals to remain on-feed longer, with extra weight compensating for shorter supplies and improving efficiency in the boning room.

The other key characteristic of tight livestock supply periods is the desire to own cattle at younger and younger ages. Backgrounding becomes critical, enabling feedlots to ‘sure up supply’. Once again, this is a strategic advantage that feedlot operators enjoy.

An important future trend is the likely increase in background feedlots, most likely on-farm, that will grow cattle for large, efficient feedlots. As the weather remains unpredictable, the role of backgrounding feedlots will grow.

Bottom line

A strong global market and subdued feed prices are key to the success of feedlot operations. Given the strategic advantage that feedlots have in ‘trading from the long side’ and the ability to background and procure at younger ages, I believe we will see ongoing healthy returns for most feedlot operators through 2026 and 2027.

A more productive Australian herd has led to these production cycles speeding up, creating further opportunities for the feedlot sector.

In conclusion, I believe we are witnessing a changing of the guard in the Australian feedlot sector, which will further strengthen the market positions of supply chain participants.

Recent and future feedlot sales at these new evaluation levels still leaves ‘money on the table’ for those investing in these assets for the future with growing export demand.

I see this period of transition as a positive for the industry, with the final make-up resulting in a stronger global footprint for Australia’s grain-fed sector.

Also Read: African Development Fund Commits $14 Million Grant To Scaling Up Climate Resilience Across The Sahel

📢 If You’re in Agriculture, Make Sure the Right People Hear Your Story.

From product launches to strategic announcements, Global Agriculture offers unmatched visibility across international agri-business markets. Connect with us at pr@global-agriculture.com to explore editorial and advertising opportunities that reach the right audience, worldwide.