How Surfactants and Adjuvants Are Reshaping Crop Protection

Guest Author: Ruchit Jani, CMD of Matangi Industries

06 July 2026, New Delhi: A spray droplet leaving a nozzle has only seconds to do its work. It must reach the leaf, stay there rather than bouncing off or running into the soil, spread across a waxy cuticle engineered by the plant to repel water, and then deliver its active ingredient before sunlight, rain, or evaporation intervene. The molecule that kills the weed or the fungus gets the credit, but the performance of that droplet is governed largely by ingredients most farmers never name. Surfactants and adjuvants are the invisible workhorses of crop protection formulations, and the pressures bearing down on the industry have made them more important, not less.

The backdrop is sobering. The Food and Agriculture Organization estimates that up to 40 percent of global crop production is lost each year to pests and diseases, with plant diseases alone draining more than USD 220 billion from the global economy and invasive insects accounting for at least USD 70 billion more. At the same time, the chemistry available to fight those losses is shrinking under regulatory review, resistance is spreading, and society wants both abundant food and a lighter environmental footprint. When you cannot simply apply more active ingredient — because of cost, regulation, or resistance — you must make every gram work harder. That is precisely what good formulation technology does.

What the terms actually mean

The vocabulary is often used loosely, so it is worth being precise. A surfactant — short for surface-active agent — is a molecule with a water-loving head and an oil-loving tail. That dual nature lets it sit at the boundary between two unlike substances and reduce the surface tension between them. Adjuvant is the broader category: any material added to a spray to improve the performance or handling of the pesticide. Every surfactant used in spraying is an adjuvant, but not every adjuvant is a surfactant. The U.S. Environmental Protection Agency frames adjuvants simply as chemicals added to a pesticide to improve its efficiency, either built into the formulation or mixed into the tank by the user.

Surfactants are classified by the electrical charge they carry. Nonionic surfactants, which carry no charge, are the most widely used in agriculture because they tolerate hard water and a wide pH range and rarely react with the active ingredient; several market analyses put them at roughly half of all agricultural surfactant volume. Anionic surfactants carry a negative charge and excel as dispersants and emulsifiers, and they remain the dominant chemistry for many established herbicide systems. Cationic surfactants, positively charged, are powerful but used cautiously because they can be harsh on plant tissue and aquatic life. Amphoteric surfactants carry both charges depending on pH and are valued where mildness and stability matter.

- Nonionic – no net charge

- Anionic – negative charge

- Cationic – positive charge

- Amphoteric – charge varies

Adjuvants split along functional lines. Activator adjuvants — the surfactants, oils, and nitrogen sources — directly enhance the biological activity of the active ingredient by improving uptake and movement into the plant. Utility adjuvants do the unglamorous but essential work of making a tank mix behave: buffering pH, suppressing foam, conditioning hard water, reducing drift, and keeping mixtures stable. In hard water, for instance, ammonium sulphate sequesters calcium and magnesium ions that would otherwise tie up glyphosate, a small chemical adjustment that can meaningfully change field results.

How they earn their keep

The mechanisms are interlocking. By lowering surface tension, a surfactant lets a droplet wet and spread across the leaf instead of beading up, increasing the contact area through which an active ingredient can be absorbed. Penetration enhancers help systemic chemistry move through the cuticle and into plant tissue. Retention and rainfastness agents keep the deposit anchored so a shower an hour after application does not wash the investment away. Drift-reduction adjuvants shift the droplet-size spectrum away from the fine particles that float off-target, an increasingly regulated concern. The cumulative effect is better spray coverage from the same volume of chemical — which is another way of saying lower dose for the same control.

These are not marginal gains. Field practice with post-emergence herbicides shows that the right adjuvant is frequently the difference between commercial control and a disappointing result, which is why so many product labels specify adjuvant use rather than leaving it to chance.

A maturing but fragmented market

Sizing these markets is genuinely difficult, and buyers should treat single headline numbers with caution. Estimates for the global agricultural surfactants market in 2024 range from roughly USD 1.4 billion to about USD 3 billion depending on how analysts draw the boundaries, with compound annual growth rates clustered between 5 and 7 percent through the end of the decade. Agricultural adjuvants, a wider category, are variously pegged between about USD 2.2 billion and USD 4.7 billion in the 2024–2025 window, again growing in the mid-single digits. The dispersion reflects methodology, not confusion about direction: the trend is steady, demand-driven growth.

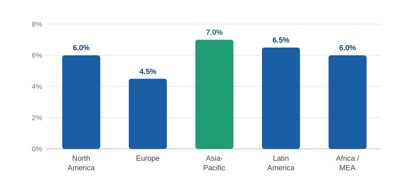

Regional patterns are clearer than absolute values. North America and Europe remain the largest and most mature markets, supported by high-value cropping, advanced application equipment, and stringent residue expectations; several analyses place North America’s share of the adjuvant market between roughly a third and 45 percent. Asia-Pacific is consistently identified as the fastest-growing region, propelled by India and China, expanding arable demand, and government productivity programmes. Latin America — Brazil in particular — is a powerful growth engine on the back of soybean and row-crop acreage, while Africa represents a long-horizon opportunity constrained today by access, awareness, and cost. Within the chemistry mix, bio-based surfactants are the fastest-growing segment in most forecasts, even as synthetic chemistries still command the large majority of volume on price and supply grounds.

Where the additives go

Herbicides remain the single largest application, typically cited at just under half of adjuvant and surfactant use, reflecting the scale of weed control across cereals, oilseeds, and row crops. Fungicides rely on surfactants for even coverage and disease suppression on fruits, vegetables, and grains, where redistribution across the canopy matters. Insecticide programmes increasingly lean on adjuvants to deliver lower doses effectively as resistance management and integrated pest management take hold.

The most consequential shift, though, is in biological crop protection. Microbial and biochemical products behave very differently from synthetic molecules — living organisms need formulations that keep them viable in storage and on the leaf — and adjuvant design has become a gating technology for the whole biologicals category. Seed treatment is another fast-growing frontier, where adjuvants govern adhesion, coverage, and the survival of biological coatings on the seed.

A regulatory landscape in motion

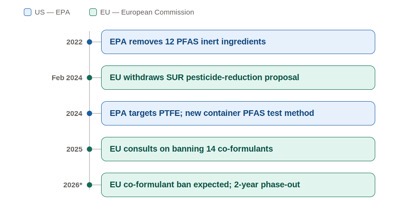

If one theme dominates the next five years, it is regulation. In the United States, the EPA finalised the removal of 12 per- and polyfluoroalkyl substances (PFAS) from its list of inert ingredients approved for non-food pesticide products, and in February 2024 moved against polytetrafluoroethylene as well, while also publishing a validated method to detect PFAS leaching from fluorinated HDPE containers. Federal oversight of stand-alone adjuvants remains comparatively light, but that gap is filled at the state level — California’s regime, which requires adjuvants to be registered as pesticides with formulation disclosure and use reporting, is the most robust in the country.

Europe is moving on a parallel but distinct track. The proposed Sustainable Use of Pesticides Regulation, which would have mandated a 50 percent cut in pesticide use and risk by 2030, was withdrawn by the European Commission in February 2024, leaving the reduction pathway uncertain. Yet the scrutiny of formulation ingredients continues: under Regulation (EC) No 1107/2009 the Commission has built a list of unacceptable co-formulants and, following a consultation that closed in October 2025, proposed banning a further 14 co-formulants from both pesticides and the adjuvants mixed with them, with adoption anticipated and a two-year withdrawal window for affected authorisations. Separately, Regulation (EU) 2024/1487 introduced EU-level data requirements for safeners and synergists. Adjuvants themselves are still authorised member state by member state, pending harmonised criteria. Underlying all of this, surfactants and co-formulants are chemicals in their own right and fall within the scope of REACH, where environmental risk and biodegradability data increasingly shape what can be sold.

The combined message to formulators is consistent across jurisdictions: ingredient identity, environmental fate, and ecotoxicity are now central to product selection, not peripheral.

The sustainability squeeze

Regulatory pressure and market demand are pulling in the same direction. Biodegradability and aquatic eco-toxicity have become design criteria rather than nice-to-haves. Renewable feedstocks are gaining ground — fermentation-derived biosurfactants such as rhamnolipids, and surfactants built from plant oils and sugars, are reaching commercial scale — partly to cut carbon footprint and partly to pre-empt the next wave of restrictions on petrochemical chemistries. Procurement signals reinforce the shift, from organic-land targets in Europe to retailer demands for residue-free produce. The OECD’s work to harmonise testing methods for biological products is, quietly, one of the more important enablers of this transition, because it lowers the cost of bringing greener chemistries to multiple markets.

What keeps formulators awake

None of this is simple to execute. Compatibility is a perennial headache: an adjuvant that boosts one active ingredient can antagonise another or destabilise a complex tank mix. Stability over shelf life and across temperature swings must be proven, especially for living biologicals. Cost-performance balance is unforgiving, particularly for price-sensitive smallholders who weigh every input. Regulatory compliance now demands data packages that did not exist a decade ago. And supply chains for specialty surfactants — many of them globally concentrated — carry their own risk.

The road to 2030

The trajectory is reasonably clear even if the numbers are not. Expect next-generation surfactants engineered for specific modes of action and lower environmental persistence; bio-based adjuvants moving from niche to mainstream; and adjuvant chemistry co-developed alongside precision application — drift-reduction and droplet-management additives tuned for drone and sensor-guided spraying that places chemical only where it is needed. Digital agriculture will increasingly inform which adjuvant to use for a given soil, crop, and weather window. Across the spectrum of forecasts, the agricultural surfactants and adjuvants markets are expected to keep compounding in the mid-single digits through the end of the decade, with biologicals-linked demand growing considerably faster.

The active ingredient will always take top billing. But in an era of fewer molecules, lower doses, and higher expectations, the chemistry that gets that molecule to its target is where much of the real innovation now lives.

Key takeaways

- Formulation is leverage. With fewer active ingredients and pressure for lower doses, surfactants and adjuvants are the primary means of extracting more efficacy from less chemical.

- The market is growing steadily but is hard to size. Credible 2024–2025 estimates span a wide range; what is consistent is mid-single-digit growth, North American and European maturity, and Asia-Pacific leading expansion.

- Regulation is the defining force. The EPA’s PFAS inert-ingredient removals and the EU’s proposed 14-co-formulant ban signal that ingredient identity and environmental fate now drive product selection.

- Biologicals depend on adjuvant science. Keeping living organisms viable from tank to leaf has made formulation a gating technology for the fastest-growing segment of crop protection.

- Green chemistry is moving from optional to expected. Biodegradability, renewable feedstocks, and harmonised testing are reshaping which surfactant chemistries have a commercial future.

Also Read: Bayer Group to Consolidate U.S. Glyphosate Business Into Distinct Entity Operating As Ruveon

Global Agriculture is an independent international media platform covering agri-business, policy, technology, and sustainability. For editorial collaborations, thought leadership, and strategic communications, write to pr@global-agriculture.com